Evidence of a soft landing in 2023 -- a short, shallow recession or no recession at all – is building.

Two of the nation’s most sensible financial economists are expecting a short, shallow recession or no recession at all.

{kind=link}

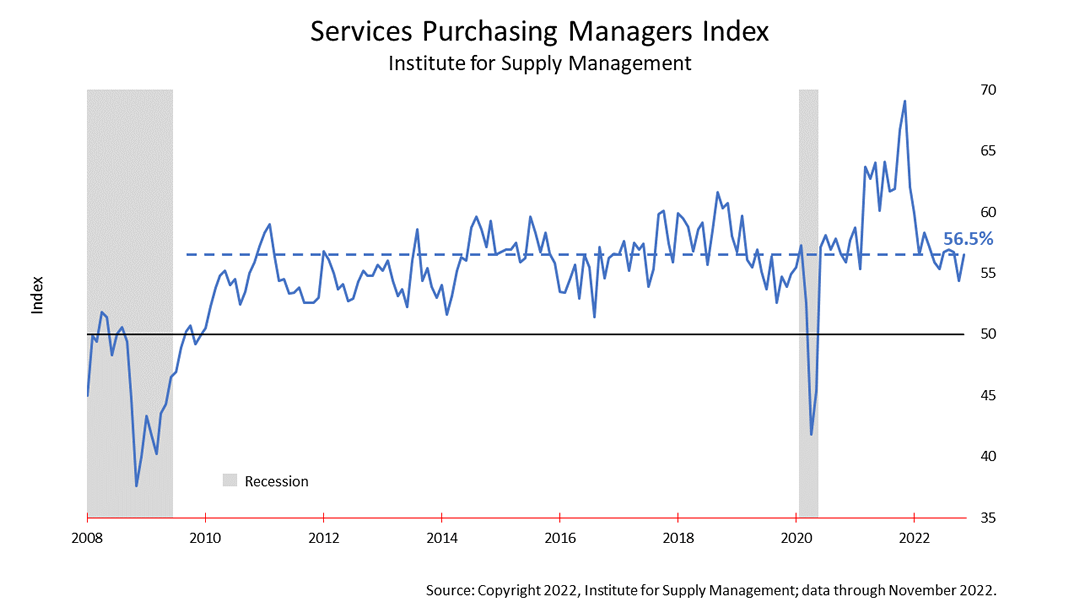

The service sector of the economy strengthened in November, according to Institute for Supply Management (ISM) data released Monday, Dec. 5.

Services comprise 89% of the U.S. economy and provide 91% of U.S. jobs, excluding jobs in farming.

At 56.5%, purchasing managers at large services companies who were surveyed reported business is as strong as was experienced in the last U.S. expansion cycle, as is highlighted by the dashed blue line.

New orders entering the pipeline at service sector companies, a key forward-looking sub-index of ISM’s service sector purchasing managers monthly data, came in at 56%.

Monthly surveys of purchasing managers conducted by the ISM are a private sector initiative relied on by business leaders, investment fiduciaries, and government policymakers in the U.S. and worldwide. They serve as a good example of the institutional strength wrought by America’s system of capitalism.

{kind=link}

More evidence of a soft landing is shown in this chart. The GDPNow forecast for growth in the current quarter, ending Dec. 31, 2022, is +3.2% .

GDPNow is an algorithm authored by the Federal Reserve Bank’s Atlanta District. It’s an attempt to estimate the final growth rate in gross domestic product in real time. As new economic reports, like ISM’s Purchasing Managers Indexes, are reported each quarter, the GDPNow forecast is updated. It was updated after the Friday morning, Dec. 9, releases from the US Census Bureau and US Bureau of Labor Statistics.

The GDPNow model estimate for real fourth quarter 2022 gross domestic product (GDP) growth is +3.2%. That would be spectacular, considering the latest consensus of leading U.S. economists is for a +1.2% growth rate this quarter.

GDPNow, as a forecasting tool, does not have a great long-term record. The human experts, professional economists surveyed regularly by Blue Chip Economics and The Wall Street Journal, more accurately forecast GDP growth in recent years. However, the algorithm has been more reliable than the humans for the past two quarters, characterized by pandemic-related anomalies.

{kind=link}

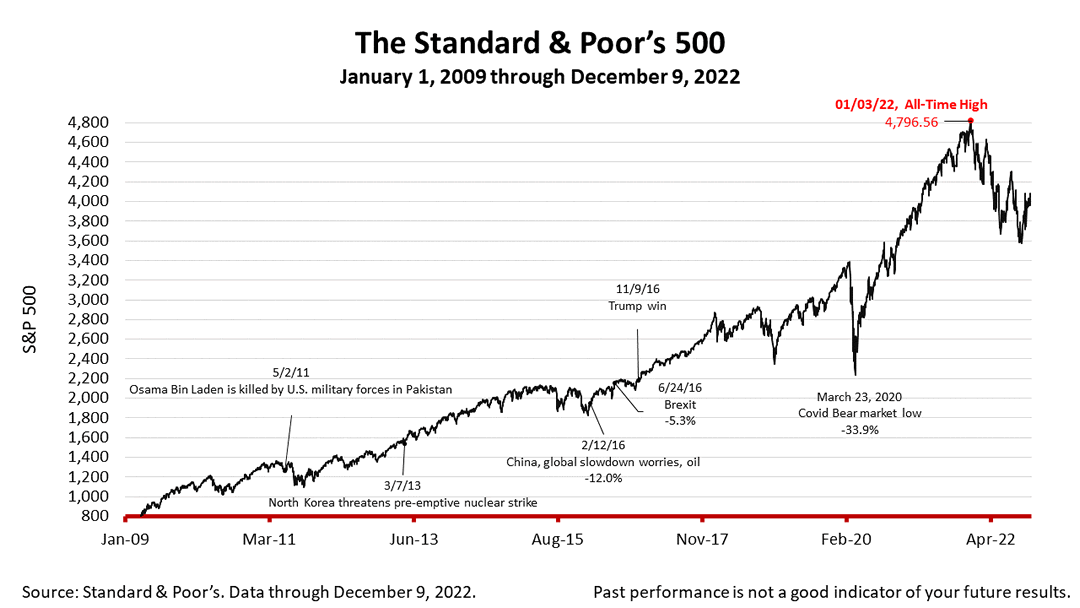

The S&P 500 stock index closed Friday at 3,934.38, losing -0.73% from Thursday and -3.37% from a week ago. The index is up +75.84% from the March 23, 2020 bear market low and 17.97% lower than its January 3rd all-time high.

The strong growth forecast from GDPNow and November’s survey of purchasing managers belie expectations by economists of a recession. But perhaps the most important consideration is that two of the nation’s most sensible financial economists are expecting a short, shallow recession or no recession at all.

Fritz Meyer, whose data and analysis are cited in this space regularly, and Ed Yardeni, a frequent guest on CNBC and one of the nation’s best-known independent economists, are saying the worst of the inflation crisis and other post-pandemic anomalies are behind us. The stock market, as measured by the S&P 500, remains nearly 20% lower than its all-time high Jan. 3, 2022, and, if Fritz and Ed are right, now is a good time to position your portfolio for the next financial economic recovery.

The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. It is a market-value weighted index with each stock's weight proportionate to its market value. Index returns do not include fees or expenses. Investing involves risk, including the loss of principal, and past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted.