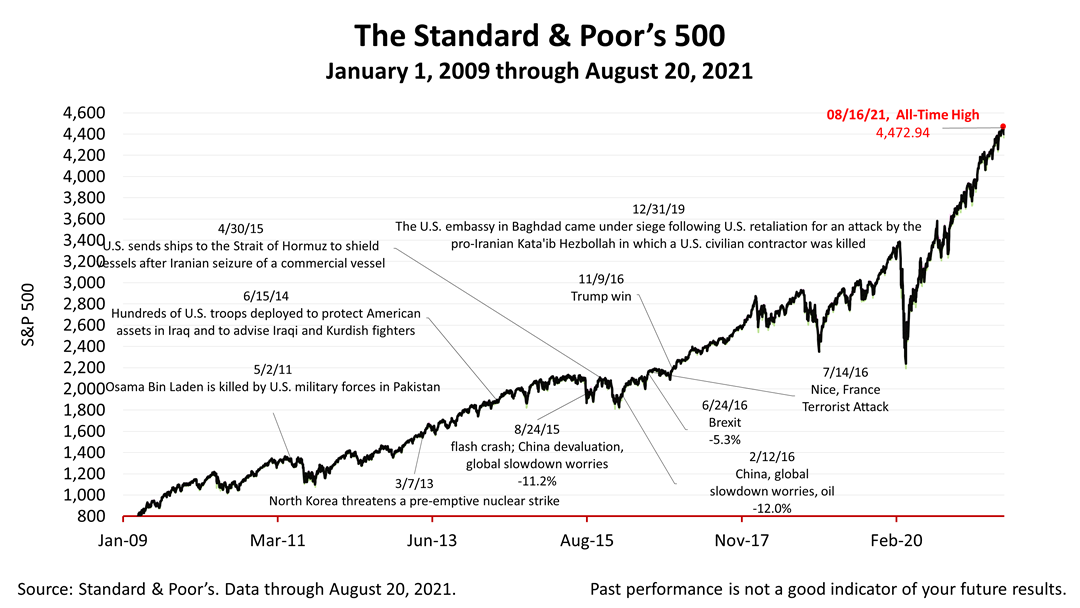

The Standard Poor's 500 stock index, the main growth driver of investor portfolios, closed the week less than 1% off Monday's all-time closing high, and the U.S. Index Of Leading Economic Indicators surged again in July. Meanwhile, the latest fundamentals, retail sales and housing starts data, remained very strong in July. Here's a two-minute update for investors.

This chart shows that the LEI has rolled over very definitively prior to recession – except for the Covid-19 recession, making it a reliable indicator of what’s ahead in the economy. The LEI’s surge since the Covid recovery began indicates no recession is in the outlook.

The Conference Board, an association for large U.S. companies, has measured the U.S. Leading Economic Indicators monthly since 1996 and the index is higher than since its inception.

“The U.S. LEI registered another large gain in July, with all components contributing positively. The Leading Index’s overall upward trend, which started with the end of the pandemic-induced recession in April 2020, is consistent with strong economic growth in the second half of the year,” according to the Conference Board’s economics research team. “While the Delta variant and/or rising inflation fears could create headwinds for the US economy in the near term, we expect real GDP growth for 2021 to reach 6% year-over-year, before easing to a still robust 4% growth rate for 2022.”

The Conference Board Leading Economic Index® (LEI), is comprised of the following component indexes measuring fundamentals key to growth in the U.S:

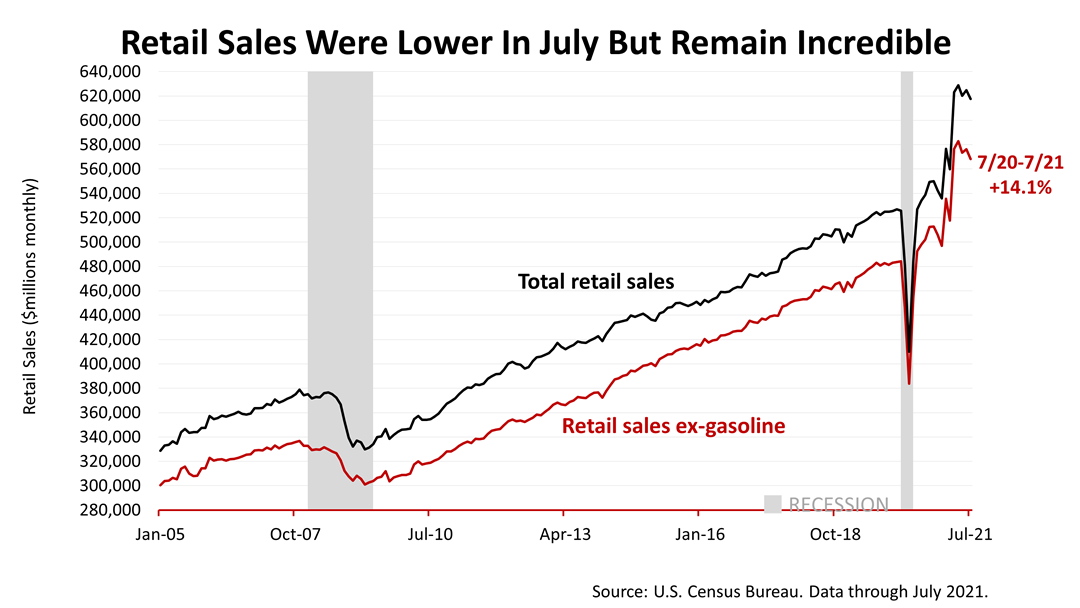

The Census Bureau’s monthly retail sales report is comprised mostly – 88% -- of sales of goods while just 12% of retail sales comes from the service sector. Retail sales overall contribute 30% of U.S. economic growth.

In July, retail sales ticked lower and some commentators say it’s a bad sign. However, retail sales are coming off a spectacular Covid recovery surge that had propelled retail sales to heights no one had expected. The 1.1% decline in retail sales that occurred from June to July was not so important in the context of the 15.6% surge in retail sales in the 12 months ended July 2021.

July retail sales excluding gasoline prices because of their volatility, are up +14.1% y/y compared to June’s +17.0% y/y.

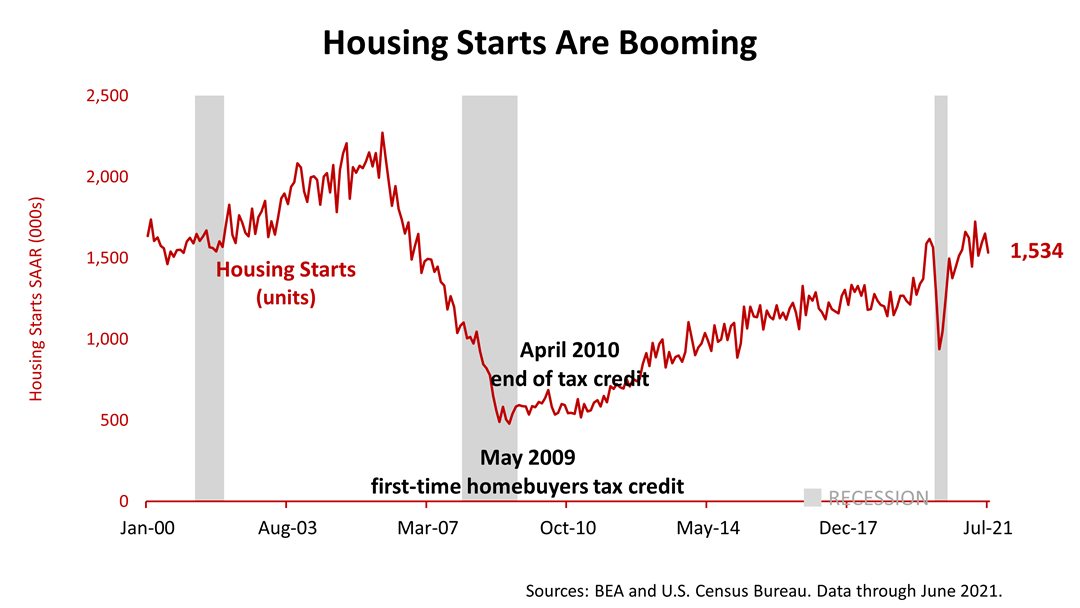

In July, the U.S. government recorded 1.53 million housing starts, compared to 1.64 million in June. That’s down from a month ago but is still near a 15-year high. The U.S. needs about 1.7 million new single-family homes built every year and had been trailing that figure for 15 years until just before the pandemic. After plunging during the initial Covid outbreak, it has staged a comeback to its pre-Covid strength.

The Standard & Poor’s 500 stock index closed today at 4,441.67. The index gained +0.81% from Thursday and is down -0.59% from last week. The index is up +66% from the March 23, 2020, bear market low.

This website uses cookies for navigation, content delivery and other functions. By using our website you agree that we can place cookies on your device. I understand